Duty paid under Protest

Duty paid under Protest

Duty paid under protest is a convention that has

been coming from old indirect tax regime. It is a common phenomenon in Excise.

Many cases were held regarding this issue. But what exactly this “duty paid

under protest” means? There might be some cases where the department will

demand the assessee for the payment of taxes which, indeed, the assessee is not

required to pay. Now, you might be wondering that why the department will

insist the tax payer to pay taxes if he is not liable. Let us see this with

some examples:

- Mr. A is a manufacturer who produces a product on which tax will be charged at 5%. But the department is of the opinion that the product was wrongly classified and it should actually be taxable at 12%. During this kind of situation, if the assessee is sure that his product is correctly classified, he may pay the tax ‘under protest’, and make an appeal to the department explaining the situation (subject to conditions in 233B).

- Mr. B is a supplier who supplies exempt goods. But the department contended that the said goods are taxable and Mr. B has to discharge the tax on the same. In this case also, assessee may pay tax ‘under protest’ and make an appeal to the department.

So, the reason could be wrong classification, wrong

computation etc., In both the above cases, the tax paid by the assessee on the

basis of department’s contention is called as ‘duty paid under protest’. So,

the assessee is paying the duty under protest of the department. After that he

has to write a letter to the proper officer stating that he has paid duty under

protest and shall make an appeal against the department. The assessee can claim

the refund of the such duty paid, if the judgement for the appeal he has made,

comes in his favour. Here you may have a doubt that why would he pay the tax

and claim the refund (if the judgement comes in his favour)? Instead why can’t

he directly file an appeal without paying the duty? Yes, he can. But the problem

is what if the judgement doesn’t come in his favour. He has to pay the tax

along with interest and penalty. To avoid this risk, the assessee will pay the

tax (under protest) first, then make an appeal and can claim refund if the

judgement is in his favour.

There is no specific provision in GST which talks

about the “refund of duty paid under protest” unlike Rule 233B of Central

Excise Rules, 1944. But, section 54(8)(e) says that “the tax and interest, if

any, or any other amount paid by the applicant, if he had not passed on the

incidence of such tax and interest to any other person”. Based on this

provision the assessee can prove that he has not passed the burden of tax onto

other person (as he would have paid the tax from his own pockets) and can claim

refund of the same.

DUTY PAID UNDER PROTEST IN EARLIER LAWS

There was a separate provision in the Central

Excise Act, 1944 which discusses about the procedure to pay duty under protest.

Rule 233B clearly specified the process regarding payment of duty under protest.

As there used to be manual process in old indirect tax regime, there were lot

of complexities and rules for paying duty under protest.

Rule 233B:

Procedure to be followed in cases where duty is paid under protest: (Central

Excise Rules,1944)

- Where an assessee desires to pay duty under protest he shall deliver to the proper officer a letter to this effect and give grounds for payment of the duty under protest.

- On receipt of the said letter, the proper officer shall give an acknowledgement to it.

- The acknowledgement so given shall, subject to the provisions of sub-rule (4), be the proof that the assessee has paid the duty under protest from the day on which the letter of protest was delivered to the proper officer.

- An endorsement "Duty paid under protest" shall be made on all copies of the gate pass, the Application for Removal and Form R.T.12 or Form R.T. 13, as the case may be.

- In cases where the remedy of an appeal or revision is not available to the assessee against any order or decision which necessitated him to deposit the duty under protest, he may, within three months of the date of delivery of the letter of protest, give a detailed representation to the Assistant Commissioner of Central Excise or Deputy Commissioner of Central Excise.

- In cases where the remedy of an appeal or revision is available to the assessee against an order or decision which necessitated him to deposit the duty under protest, he may file an appeal or revision within the period specified for filing such appeal or revision, as the case may be.

- On service of the decision on the representation referred to in sub-rule (5) or of the appeal or revision referred to in sub-rule (6) the assessee shall have no right to deposit the duty under protest:Provided that an assessee shall be allowed to deposit the duty under protest during the period available to him for filing an appeal or revision, as the case may be, and during the pendency of such appeal or revision, as the case may be.

- If any of the provisions of this rule has not been observed, it shall be deemed that the assessee has paid the duty without protest.

Note: -A letter of protest or a

representation under this rule shall not constitute a claim for refund.

Simplifying Rule 233B

- If the assessee desires to pay duty under protest, he shall deliver a letter to the proper officer i.e., Assistant Commissioner of Central Excise or Deputy Commissioner of Central Excise stating the grounds for such payment.

- Such proper officer shall give an acknowledgement which is duly signed and sealed.

- This acknowledgement will act as proof that the assessee has paid tax under protest.

- Then the assessee shall state the fact, on Application for removal, Form RT12 or Form RT13, that the duty was paid under protest. Generally, a stamp stating “Refund paid under Protest” will be affixed on such forms.

- If the assessee doesn’t have option to file an appeal, he can give a detailed representation to Assistant Commissioner of Central Excise within 3 months.

- If the assessee have option to file an appeal, he can file such appeal within specified time.

- After the decision of such representation or appeal, the assessee shall have no right to deposit duty under protest. But the assessee can deposit such duty under protest during period available for filing appeal (sub rule 6) and during the period where appeal is made but the judgement is pending. But after the judgement he cannot deposit such duty. The reason could be:

a.

If judgement is his favour – No need to pay tax

b.

If judgement is not in

favour – Assessee can further appeal to the higher

authorities. But, if the appeal is at the stage of finality and still the

judgement is not in his favour, it becomes regular tax and not duty paid under

protest. The assessee has to discharge the tax liability along with interest

and penalty.

Explanation to the Note:

At the end of the rules it is clearly mentioned

that “a letter of protest or a representation under this rule shall not

constitute a claim for refund” which means you cannot file refund of duty paid

under protest based on mere representation or letter of protest you have

submitted to the officer. If the judgement is in the favour of assessee, you

have to file a refund application stating that you have paid tax under protest

and claim refund as per section 11B of The Central Excise Act, 1944.

Central Excise Rules, 2002:

In the year

2002, Excise department has amended its rules by introducing “The Central

Excise Rules, 2002”. This time, no corresponding provision or rule has been

included regarding “duty paid under protest”. But later CBEC has provided some

supplementary instructions in its manual describing the procedure to be

followed for paying duty under protest, which is as follows:

- The assessee shall inform the Superintendent or Inspector of Central Excise in writing giving reasons for paying duty under protest and a dated acknowledgement will be given to him.

- He will mark invoices or monthly/quarterly return indicating the goods on which duty is paid “under protest”. If a lump-sum duty payment in respect of past demand, he may record the fact of duty payment under protest in the Personal Ledger Account, CENVAT Account and Daily Stock Account.

- If a case is applied against by the assessee or where the appeal period for further appeal is available, he may continue to pay duty under protest. However, if decision is not in his favour and he exhausts the appellate remedy or doesn’t appeal within stipulated time, the assessee shall not have any right to pay duty under protest.

As we can see

that the procedure mentioned in Rule 233B of Central Excise Rules, 1944 and in

supplementary instructions of the Central Excise Act, 2002 are similar and in

the new rules they have just simplified the process.

DUTY PAID UNDER PROTEST IN GST LAW

Central Goods and Service Tax Act, 2017:

This is our

primary concern now. How to deal with “duty paid under protest” in GST?

Unfortunately, there is no provision under CGST Act or Rules regarding this issue.

This is the reason I’ve mentioned that what the previous laws are saying. Even

though, the procedure regarding duty paid under protest has been listed in

Central Excise, the same procedure was used by the tax payers of Customs Act

and Service Tax. As there is no procedure laid down in GST, we can apply the

old process for paying duty under protest and if the judgement is in favour of

assessee, he can file refund based on section 54(8)(e), which says that “the tax and

interest, if any, or any other amount paid by the applicant, if he had not

passed on the incidence of such tax and interest to any other person”. As he

would have paid tax from his own pockets, he can prove that he has not passed

the burden of tax and claim refund of the same.

Furthermore, duty paid

under protest is an integral part of “principle of natural justice”. Payment of

duty under protest means challenging the issue on merits. Not accepting the

circular or order seeking natural justice and contesting is the fundamental

right of the assessee. So, nobody can snatch such right from him. Even if there

is no provision in CGST Act, 2017 on payment of duty under protest, as a matter

of justice, he can pay such duty under protest, if he wishes so.

Section 174(2)(c) of

CGST Act, 2017 also says that the repeal of Central Excise Act, 1944 shall not

affect any right, privilege, obligation or liability incurred under such

repealed act or orders under such repealed acts. Provided that any tax

exemption granted as an incentive against investment through notification shall

not continue as privilege if the said notification is rescinded. So, paying

duty under protest is a privilege and appealing against that is a right given

to the assessee, which have not been rescinded under any notification in the

GST law. So, that tax payers still can pay duty under protest and contest the

same.

Now the biggest

question here arises is, can the assessee apply Rule 233B of Central Excise

Rules, 1944 or the procedure mentioned in supplementary instructions of Central

Excise Act, 2002 (both are similar indeed) which talks about the procedure of paying

duty under protest, for GST cases?

As there is no

specific procedure mentioned under GST law, we can suggest the assessees to pay

duty under protest using the procedure mentioned in old law, till there is any

specific provision under GST. But, still it is opined that there should be a

provision regarding this issue in GST law.

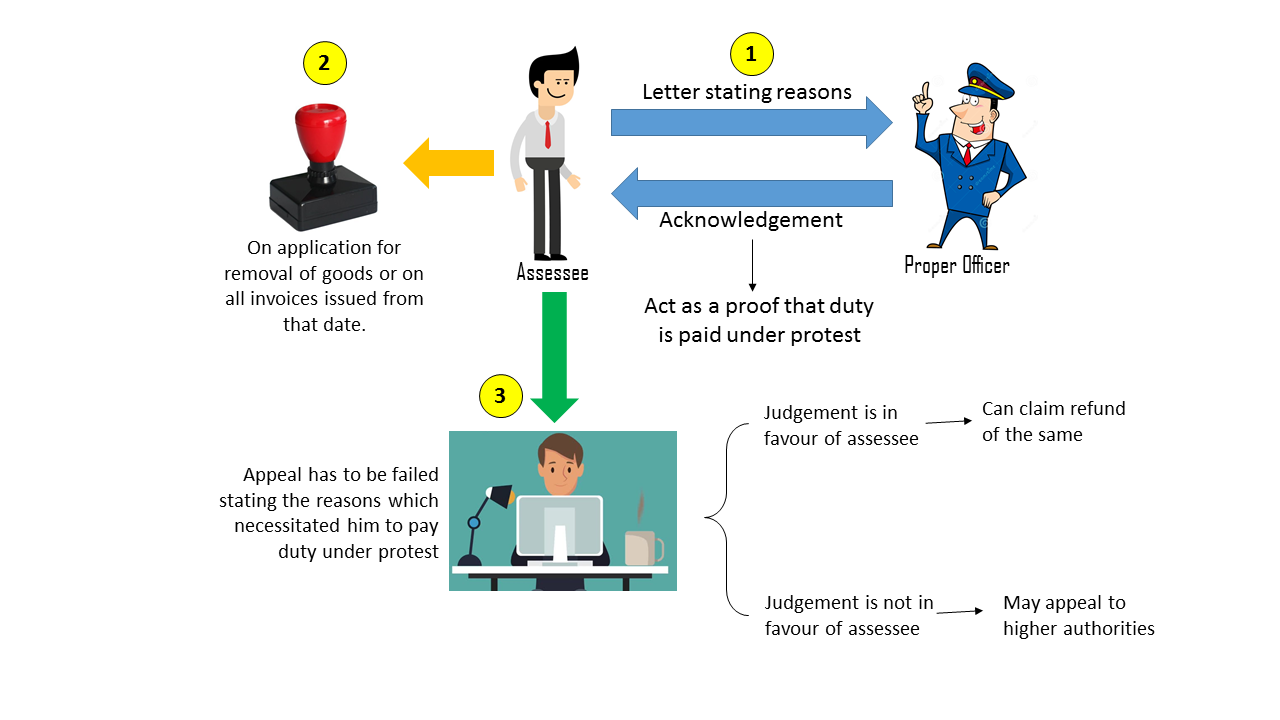

Procedure for paying duty under protest in GST

- Write a letter to the jurisdictional GST range officer with a copy to the Deputy Commissioner who is in charge of GST division.

- Mention the details of amount paid under protest, challan number etc., and state the fact that “This payment has been made under protest. We do not agree with the views of the department. We shall contest the issue before appellant authority”.

- Get an acknowledgement along with sign and stamp of the office, along with name of dealing official mentioned therein.

- Mark all the invoices issued, returns filed thereafter with a stamp “duty paid under protest”.

- File an appeal with the tribunal stating the reasons which necessitated him to pay tax under protest.

Recent Case of Yes Bank Ltd.

Recently a case

has been held relating to Yes Bank Ltd where the department has raised certain

observation regarding the computation of GST liability on transactions

pertaining to Domestic Money Transfer and computed the amount of Rs. 38.04

crore liability which is to be payable. Yes Bank has paid the tax as per department’s

contention and posted in its website, a press release stating that they have

paid GST amounting to Rs. 38.04 crore “under protest”

Duty paid under Protest

Reviewed by Vinay Kumar

on

March 12, 2020

Rating:

Reviewed by Vinay Kumar

on

March 12, 2020

Rating:

Reviewed by Vinay Kumar

on

March 12, 2020

Rating: